#Loan refinancing benefits

Explore tagged Tumblr posts

Visit Tumblr Blog

Explore Tumblr blogs with no restrictions, modern design and the best experience.

Last Seen Tumblr Blogs

Fun Fact

Average visit duration of Tumblr.com is 10 mins and 25 secs.

Text

How to Create a Financial Plan for Personal Loan Repayment?

A personal loan can be a great financial tool to manage unexpected expenses, fund major purchases, or consolidate debt. However, repaying the loan on time is crucial to maintaining financial stability and a good credit score. Without a well-structured financial plan, borrowers may struggle with high EMIs, increasing debt burden, and late payment penalties.

In this guide, we will walk you through the essential steps to create an effective financial plan for personal loan repayment. By following these strategies, you can ensure timely payments, reduce financial stress, and even save on interest costs.

1. Assess Your Current Financial Situation

Before creating a loan repayment plan, take a close look at your financial standing. Analyze:

✔ Total outstanding loan amount – Check how much of your personal loan is still unpaid. ✔ Monthly income sources – Identify your salary, freelance earnings, or passive income. ✔ Existing expenses – List fixed costs such as rent, utilities, and daily expenses. ✔ Other financial commitments – Include credit card dues, other loans, or savings goals.

How This Helps:

Knowing your income and expense balance allows you to set a realistic repayment strategy without overburdening your finances.

2. Choose the Right EMI Structure

Banks and NBFCs (Non-Banking Financial Companies) offer different EMI (Equated Monthly Installment) options based on loan tenure and interest rates. Choosing the right EMI structure can impact your repayment ability.

Types of EMI Options:

✔ Fixed EMI – The EMI remains the same throughout the loan tenure. ✔ Step-Up EMI – Lower EMIs at the start, which gradually increase over time. ✔ Step-Down EMI – Higher EMIs in the beginning, reducing over time.

How to Choose:

If your income is stable, a fixed EMI is ideal.

If you expect future salary hikes, a step-up EMI might be beneficial.

If you want to clear the debt quickly, a step-down EMI reduces interest outgo.

3. Set a Monthly Budget for Loan Repayment

Once you decide on your EMI, incorporate it into a monthly budget to ensure on-time repayment.

Steps to Create a Loan Budget:

✔ Allocate 30-40% of your income towards loan repayments. ✔ Cut back on unnecessary expenses like luxury purchases or frequent dining out. ✔ Prioritize essential expenses, such as rent, groceries, and utility bills. ✔ Avoid taking on new debt while repaying your existing personal loan.

💡 Pro Tip: Use budgeting apps or an Excel sheet to track expenses and ensure EMI payments are made on time.

4. Consider Making Prepayments to Reduce Interest Costs

If you have surplus funds, consider prepaying your personal loan to lower the outstanding principal and reduce interest payments.

Benefits of Prepayment:

✔ Reduces total interest payable over the loan tenure. ✔ Shortens the loan duration, helping you clear debt faster. ✔ Improves your credit score, making future loan approvals easier.

Things to Check Before Prepaying:

✔ Confirm whether your lender charges prepayment penalties (some banks charge 1-3% of the outstanding amount). ✔ Choose the right time – Prepaying early in the loan tenure gives the highest interest savings.

5. Create an Emergency Fund to Avoid Loan Defaults

Unexpected expenses like medical emergencies, job loss, or urgent home repairs can impact loan repayment. To prevent missing EMIs, set up an emergency fund.

How to Build an Emergency Fund:

✔ Save 3 to 6 months’ worth of expenses in a separate savings account. ✔ Use high-interest savings accounts or liquid mutual funds for quick access. ✔ Avoid using your emergency fund for discretionary expenses.

Having an emergency fund ensures that you can continue EMI payments even during financial setbacks.

6. Consider a Loan Balance Transfer for Lower Interest Rates

If your current personal loan has a high-interest rate, refinancing it through a loan balance transfer can help you reduce EMI payments.

Steps for a Loan Balance Transfer:

✔ Compare interest rates from different banks or NBFCs. ✔ Check for processing fees or balance transfer charges. ✔ Ensure that the new lender offers lower EMIs or better loan terms. ✔ Transfer the remaining loan amount to the new lender and enjoy reduced interest costs.

This strategy can help you save thousands in interest payments over time.

7. Use Windfalls or Bonuses for Repayment

If you receive a salary bonus, tax refund, or unexpected cash inflow, consider using a part of it to repay your personal loan.

Why Use Windfalls for Loan Repayment?

✔ Reduces outstanding loan balance and lowers EMI burden. ✔ Helps you become debt-free faster. ✔ Saves on total interest costs over the loan tenure.

Instead of spending bonus money on luxury purchases, use it for loan prepayment to improve financial stability.

8. Set Up Auto-Debit for EMI Payments

Late payments not only attract penalties but can also damage your credit score. To ensure timely EMI payments, set up an auto-debit feature with your bank.

Benefits of Auto-Debit for Loan EMIs:

✔ Avoids late payment penalties. ✔ Reduces the risk of missing EMI deadlines. ✔ Keeps your credit score intact.

Ensure that your bank account always has sufficient funds before the EMI due date to prevent auto-debit failures.

9. Avoid Taking Additional Debt During Repayment

Taking new loans while repaying your existing personal loan can increase financial pressure.

Why Avoid Multiple Loans?

✘ Increases monthly debt obligations. ✘ Affects your Debt-to-Income (DTI) ratio, reducing future loan eligibility. ✘ May result in higher interest rates on future borrowings.

Instead of taking on new loans, focus on repaying your current personal loan before considering new financial commitments.

10. Track Your Loan Repayment Progress Regularly

Monitor your loan repayment progress to ensure you are on track.

How to Track Loan Repayment:

✔ Check your loan statement regularly to see outstanding balance and interest paid. ✔ Use a loan EMI calculator to estimate prepayment benefits. ✔ Contact your lender to understand any modifications or restructuring options.

Tracking your progress helps you stay motivated and make adjustments to your financial plan if needed.

Final Thoughts: Stay Disciplined for a Debt-Free Future

Repaying your personal loan doesn’t have to be overwhelming. By creating a structured financial plan, you can:

✔ Make timely EMI payments. ✔ Reduce total interest costs. ✔ Improve your credit score. ✔ Become debt-free faster.

Following the above strategies will help you manage your personal loan repayment efficiently and achieve long-term financial stability.

#personal loan online#fincrif#loan apps#nbfc personal loan#personal loans#loan services#personal laon#personal loan#finance#bank#Personal loan#Loan repayment plan#Personal loan EMI#Debt repayment strategy#Loan prepayment#Loan balance transfer#Personal loan interest rate#Personal loan tenure#Loan repayment schedule#Personal loan EMI calculator#How to repay a personal loan#Debt management tips#Budget for loan repayment#EMI auto-debit#Loan prepayment penalty#Personal loan default impact#How to save on loan interest#Best way to repay a personal loan#Loan refinancing benefits#Debt-to-income ratio improvement

1 note

·

View note

Text

0 notes

Text

Decoding your Dream Home: A Simple Guide to Calculating Your Home Loan EMI

Owning a home - it's the cornerstone of Indian dreams, a symbol of stability and success. But navigating the financial intricacies of a home loan can feel like deciphering hieroglyphics. Enter the Home Loan EMI Calculator, your trusty decoder ring in this financial adventure.

What's this magical calculator, you ask? Imagine a genie who grants your wish to know your monthly payment (EMI) before you even sign on the dotted line. That's the Home Loan EMI Calculator! But to truly wield its power, let's crack the code on a few key terms:

EMI (Equated Monthly Installment): The fixed amount you pay towards your loan every month, like a delicious bite-sized piece of your dream home pie.

Interest Rate: The cost of borrowing the money, like the sprinkles on your pie - some like it sweet, some prefer less!

So, how does this EMI magic work? Buckle up, we're going on a formula field trip!

The EMI Formula: P x R x (1 + R)n / ((1 + R)n - 1)

Don't faint! We'll break it down:

P: Loan amount - Your desired palace size.

R: Interest rate - Sweet or not-so-sweet sprinkles.

n: Loan tenure - How many years to savor your pie.

Steps to Master the EMI Spell:

1. Gather your Loan Details: Know your desired loan amount and preferred tenure.

2. Uncover the Interest Rate: Consult lenders or use online resources to compare rates.

3. Channel your Inner Mathematician: Plug your details into the formula, or use the magic of online EMI calculators.

4. Embrace the Amortization Schedule: This table unveils how your payments chip away at the principal and interest over time.

Beyond the EMI Spell:

1. Home Loan Insurance: Shield your loved ones with this protective charm.

2. Tax Benefits: Enjoy tax deductions on your EMIs - like finding extra sprinkles in your pocket!

3. Refinancing Options: If interest rates dip, consider recasting your spell for a sweeter deal.

Remember, SRG Housing, your friendly neighborhood housing finance wizards, are here to guide you through every step. We specialize in empowering the underserved to turn their dream homes into reality. Contact us today and let's unlock your EMI magic together!

We are committed to empowering individuals in rural and semi-urban areas of India to realize their dream of owning a home. Explore your possibilities with SRG Housing.

Visit www.srghousing.com to unlock your dream home's EMI magic!

#home loan emi calculator#Equated Monthly Installment#Interest rate#Loan amount#Loan tenure#EMI formula#Home loan insurance#Tax benefits#Refinancing options#SRG Housing#Housing finance

0 notes

Text

{ MASTERPOST } Everything You Need to Know about Saving Money and Being Frugal

We’re all in this together. Don’t give up.

On food and groceries:

How to Shop for Groceries like a Boss

Why Name Brand Products Are Beneath You: The Honor and Glory of Buying Generic

If You Don’t Eat Leftovers I Don’t Even Want to Know You

You Are above Bottled Water, You Elegant Land Mermaid

You Should Learn To Cook. Here’s Why.

On entertainment and socializing:

The Frugal Introvert’s Guide to the Weekend

7 Totally Reasonable Ways To Save Money on Cheap Entertainment

Take Pride in Being a Cheap Date

The Library Is a Magical Place and You Should Fucking Go There

Your Library Lets You Stream Audiobooks and eBooks FOR FREEEEEEE!

What’s the Effect of Social Media on Your Finances?

You Won’t Regret Your Frugal 20s

On health:

How to Pay Hospital Bills When You’re Flat Broke

Run With Me if You Want to Save: How Exercising Will Save You Money

Our Master List of 100% Free Mental Health Self-Care Tactics

Why You Probably Don’t Need That Gym Membership

How to Get DIRT CHEAP Pet Medication, Without a Prescription

On other big expenses:

Businesses Will Happily Give You HUGE Discounts if You Ask This Magic Question

Understand the Hidden Costs of Travel and Avoid Them Like the Plague

Other People’s Weddings Don’t Have to Make You Broke

You Deserve Cheap, Fake Jewelry… Just Like Coco Chanel

3 Times I Was Damn Grateful for My Emergency Fund (and Side Income)

When (and How) to Try Refinancing or Consolidating Student Loans

The Real Story of How I Paid Off My Mortgage Early in 4 Years

Season 2, Episode 2: “I’m Not Ready to Buy a House—But How Do I *Get Ready* to Get Ready?”

The Most Impactful Financial Decision I’ve Ever Made… and Why I Don’t Recommend It

On buying secondhand and trading:

Almost Everything Can Be Purchased Secondhand

I Am a Craigslist Samurai and so Can You: How to Sell Used Stuff Online

The Delicate Art of the Friend Trade

On giving gifts and charitable donations:

How Can I Tame My Family’s Crazy Gift-Giving Expectations?

In Defense of Shameless Regifting

Make Sure Your Donations Have the Biggest Impact by Ruthlessly Judging Charities

The Anti-Consumerist Gift Guide: I Have No Gift to Bring, Pa Rum Pa Pum Pum

How to Spot a Charitable Scam

Ask the Bitches: How Do I Say “No” When a Loved One Asks for Money… Again?

On resisting temptation:

How to Insulate Yourself From Advertisements

Making Decisions Under Stress: The Siren Song of Chocolate Cake

The Magically Frugal Power of Patience

6 Proven Tactics for Avoiding Emotional Impulse Spending

On minimalism and buying less:

Don’t Spend Money on Shit You Don’t Like, Fool

Everything I Know About Minimalism I Learned from the Zombie Apocalypse

Slay Your Financial Vampires

The Subscription Box Craze and the Mindlessness of Wasteful Spending

On saving money:

How To Start Small by Saving Small

Not Every Savings Account Is Created Equal

The Unexpected Benefits (and Downsides) of Money Challenges

Budgets Don’t Work for Everyone—Try the Spending Tracker System Instead

From HYSAs to CDs, Here’s How to Level Up Your Financial Savings

Season 2, Episode 10: “Which Is Smarter: Getting a Loan? or Saving up to Pay Cash?”

The Magic of Unclaimed Property: How I Made $1,900 in 10 Minutes by Being a Disorganized Mess

We will periodically update this list with newer articles. And by “periodically” I mean “when we remember that it’s something we forgot to do for four months.”

Bitches Get Riches: setting realistic expectations since 2017!

Start saving right heckin’ now!

If you want to start small with your savings, consider signing up for an Acorns account! They round up your every purchase to the nearest dollar and save and invest the change for you. We like them so much we’ve generously allowed them to sponsor us with this affiliate link:

Start investing today with Acorns

#frugal#saving money#personal finance#money tips#financial tips#financial literacy#financial freedom#money#debt#money management#how to save money

864 notes

·

View notes

Text

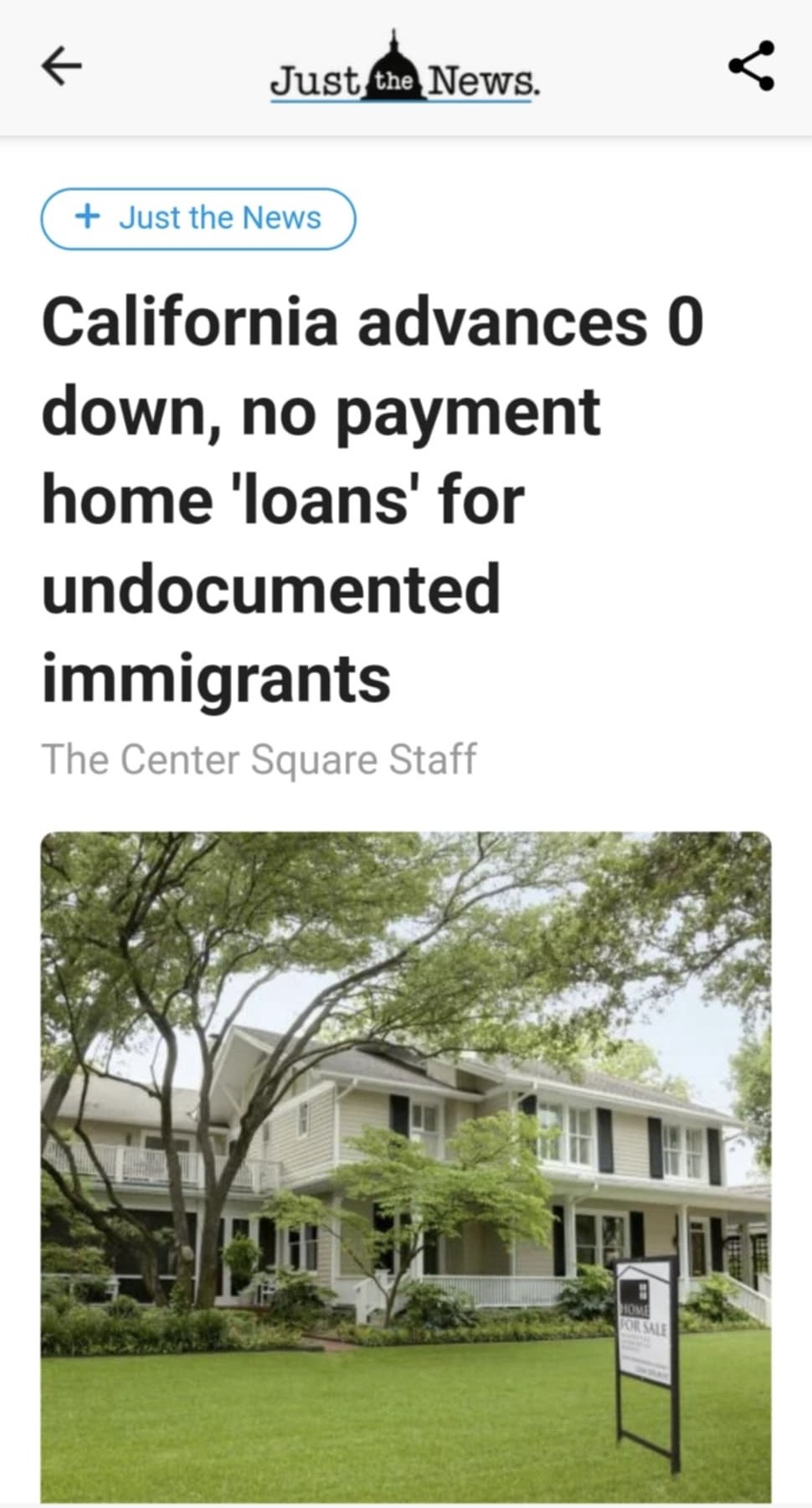

The Center Square) - The California Senate Appropriations Committee advanced a bill to allow undocumented immigrants to make use of the state’s zero down, no payment home “loan” program, an expansion the legislature says would create “significant cost pressures.”

“The social and economic benefits of homeownership should be available to everyone. As such, the California Dream for All Program should be available to all,” wrote bill author Assemblymember Joaquin Arambula, D-Fresno. “When undocumented individuals are excluded from such programs, they miss out on a crucial method of securing financial security and personal stability for themselves and their families.”

6 notes

·

View notes

Text

VA Loan Help at Your Fingertips – VALoanEducator

Get the most out of your VA loan benefits with VALoanEducator! Our app simplifies the process, helping you check eligibility, calculate payments, and understand key steps to securing a VA home loan. Whether buying or refinancing, we're here to guide you. Download now on Android & iOS!

2 notes

·

View notes

Text

Refinancing vs. Staying Put: What's Best for NZ Homeowners?

For New Zealand homeowners, deciding whether to refinance or stick with their current mortgage depends on several factors. Refinancing Mortgages can offer benefits such as lower interest rates, reduced monthly payments, or access to home equity for renovations. With fluctuating interest rates, 2024 may present opportunities for homeowners to lock in better deals, especially if current rates have decreased since their initial loan.

However, staying put can also be advantageous, particularly if breaking the existing loan incurs high penalties. Some homeowners may value stability over potential savings, especially if they have a fixed-rate mortgage and are close to the end of their term.

Ultimately, the choice comes down to personal financial goals. Refinancing may be a smart move if the long-term savings outweigh the costs, but for others, maintaining their current mortgage could provide peace of mind. Consulting a mortgage advisor can help weigh the options effectively.

#refinancemortgage#refinancing nz#home loan deposit nz#home loan#first time home buyer#new zealand#mortgage broker#refinance Auckland

3 notes

·

View notes

Text

Expert Advice on Selecting a Mortgage Consultant in UAE

Introduction to Mortgage Consulting in UAE

Selecting the right mortgage consultant is a crucial step in securing the best mortgage terms and making informed decisions. This guide provides expert advice on how to choose the best mortgage consultant in the UAE.

For more information on home loans, visit home loan dubai.

The Importance of a Mortgage Consultant

A mortgage consultant can provide expert guidance, save you time, and help you find the best mortgage products. Their role includes:

Assessing Your Financial Situation: Understanding your financial health and mortgage needs.

Exploring Mortgage Options: Identifying and comparing different mortgage products.

Negotiating Terms: Securing the best rates and terms from lenders.

Managing Paperwork: Handling all necessary documentation and processes.

For property purchase options, explore Buy Villas in Dubai.

Expert Tips for Selecting a Mortgage Consultant

Research and Recommendations: Start by researching online and seeking recommendations from trusted sources. Use online platforms to read reviews and gather information about various mortgage consultants.

Verify Credentials: Ensure the consultant is licensed and has a proven track record. Look for certifications from recognized institutions and membership in professional organizations.

Experience Matters: Choose a consultant with extensive experience in the UAE mortgage market. Experienced consultants are more likely to have established relationships with lenders and a deeper understanding of the market.

Client Reviews: Read client reviews and testimonials to gauge satisfaction and service quality. Look for patterns in feedback to identify the consultant’s strengths and weaknesses.

Clear Communication: Ensure the consultant communicates clearly and keeps you informed throughout the process. Good communication is essential for a smooth and transparent mortgage process.

For mortgage options, consider Best Mortgage Services.

Questions to Ask a Mortgage Consultant

When interviewing potential mortgage consultants, ask the following questions:

What is your experience in the UAE mortgage market? Understanding their level of experience can give you confidence in their ability to handle your case.

What types of loans do you specialize in? Some consultants may have more experience with certain types of loans, such as first-time homebuyer programs or refinancing.

How do you help clients secure the best mortgage rates? This question helps you understand their approach to negotiating with lenders.

What are your fees, and how are they structured? Transparency about fees is crucial to avoid any surprises later on.

Can you provide references from previous clients? References can provide insight into the consultant's reliability and effectiveness.

For rental options, visit Apartments For Rent in Dubai.

Benefits of Working with a Mortgage Consultant

Working with a mortgage consultant offers several advantages, including:

Access to a Wide Range of Products: Mortgage consultants have access to a broad range of mortgage products from different lenders, increasing your chances of finding the best deal.

Expert Guidance: Consultants provide expert advice on the best mortgage options based on your financial situation.

Time Savings: By handling the research, paperwork, and negotiations, consultants save you time and effort.

Stress Reduction: Managing the complexities of the mortgage process can be stressful. A consultant can alleviate this stress by guiding you through each step.

Customized Solutions: Consultants offer personalized mortgage solutions tailored to your specific needs and goals.

For property sales, visit Sell Your Property in Dubai.

Real-Life Success Story

Consider the case of Alex, a first-time homebuyer in Dubai. By following expert advice, Alex found a highly recommended mortgage consultant who helped him navigate the mortgage process, resulting in a favorable mortgage rate and a smooth home purchase.

Alex was initially overwhelmed by the various mortgage options and the paperwork involved. He decided to seek the help of a mortgage consultant based on recommendations from friends and online reviews. The consultant assessed Alex's financial situation, explained the different mortgage products available, and helped him choose the best one for his needs.

Throughout the process, the consultant handled all the paperwork, negotiated with lenders to secure a competitive rate, and kept Alex informed at every step. This personalized service made a significant difference, reducing Alex's stress and ensuring a smooth and successful home purchase.

Conclusion

Selecting the right mortgage consultant in the UAE is crucial for securing the best mortgage terms and making informed decisions. By following the expert tips outlined in this guide and conducting thorough research, you can find a consultant who meets your needs and helps you achieve your homeownership goals. For more resources and expert advice, visit home loan dubai.

2 notes

·

View notes

Text

Home Loan EMI Calculator: How to Reduce Your Home Loan EMI Burden

Buying a home is a wish that each of us has in our hearts. But as amazing as owning your own home, it is a solution that requires a large amount of investment. This investment usually includes a home loan that is gradually repaid back to the lender in the form of Home Loan EMI. Availing a home loan requires prior planning because it includes a relatively long tenure. It can weigh on household finances for a long time. An honest idea to calculate your EMI amount before signing on the line. A great tool like the Home Loan EMI Calculator can assist you out with this.

What is Home Loan EMI Calculator?

The Home Loan EMI Calculator is an online tool for calculating monthly EMI. Based on some details about home loans, the calculator will give you the exact amount EWI has to pay. It also includes a chart showing the payment schedule and details of the total payment.

Calculate Home Loan Eligibility

Advantages of Home Loan EMI Calculator

The Home Loan EMI Calculator is an all-purpose, simple, and seamless calculator that only requires you to enter 3 values. Attaining benefits is like being aware of what you are getting into. You have a clear picture of the amount of the loan that will be given to you, for how many months/years, the interest will generally be compensated. This way you can plan all your finances in advance.

With that in mind, you need to plan in advance where you will start paying the initial amount as well as the monthly EMI, which again is a task in itself.

How to Reduce Your Home Loan EMI Burden?

In a time when the fragile economy is weighing on the lives of most people, making regular loan payments is a challenge. For those who have taken out home loans where the EMI is very high, this challenge is even more difficult.

Reducing EMI payments seems like an effective way to survive in a bad economy. If, as a borrower, you’re also looking for ways to simplify your home loan by reducing your EMI payments, follow these tips-

Change your lender

When you take out a loan, you may have chosen a lender that offers you high-interest rates on your home loan. Now, when you’ve found a new lender who wants to offer significantly lower interest rates, consider replacing your lender’s middle loan. Even if you can’t find a lender with a lower interest rate on your home loan, you should look for a lender who wants to extend your repayment period. Before switching lenders, use an online home loan EMI calculator to find out how much your EMI could drop.

Changing lenders is very convenient. All you have to do is contact your existing and new lenders and request a loan balance transfer. Refinancing a home loan at a lower interest rate is one of the easiest ways to reduce EMI.

2 notes

·

View notes

Text

Mortgage Brokers in Pimpama A Must Home Review

Pimpama, a picturesque suburb in Queensland, has witnessed a surge in the real estate market, attracting homebuyers from all walks of life. Navigating the complexities of mortgages in such a thriving market can be daunting. That’s where Must Home, the leading mortgage broker in Pimpama, steps in to simplify the process.

What Sets Must Home Apart

1. Tailored Financial Solutions: Must Home prides itself on offering personalized mortgage solutions tailored to individual needs and financial situations. Their expert brokers meticulously analyze your requirements, ensuring you get the best-suited mortgage plan.

2. Comprehensive Market Knowledge: With an in-depth understanding of the local real estate landscape, Must Home brokers provide valuable insights. They help clients make informed decisions, ensuring they secure the most advantageous mortgage deals available.

3. Streamlined Application Process: Must Home simplifies the often labyrinthine mortgage application process. Their team guides you through every step, from document preparation to submission, making the journey seamless and stress-free.

4. Competitive Interest Rates: Must Home collaborates with various lenders, granting access to an array of mortgage products at competitive interest rates. This ensures clients not only find a suitable mortgage but also save significantly over the loan term.

5. Exceptional Customer Service: Beyond securing mortgages, Must Home excels in customer service. Their dedicated brokers provide ongoing support, addressing queries and concerns promptly. This commitment to client satisfaction sets them apart in the industry.

How Must Home Can Help You

Whether you’re a first-time homebuyer, looking to refinance, or investing in property, Must Home offers a diverse range of services.

First Home Buyer Loans: Must Home assists newcomers in navigating the complexities of securing their first home, ensuring they benefit from government incentives and affordable repayment plans.

Refinancing Solutions: For existing homeowners, Must Home evaluates your current mortgage, exploring opportunities for refinancing that could lead to substantial savings over time.

Investment Property Loans: Investors receive tailored financial guidance, helping them expand their real estate portfolios strategically.

Conclusion —

In conclusion, Must Home stands out as a reliable and client-focused mortgage broker in Pimpama. Their commitment to personalized service, market expertise, and exceptional customer care makes them the go-to choice for anyone seeking a mortgage solution in this vibrant suburb.

Connect with us now on +61 468 784 663 and step ahead to a wise decision .

4 notes

·

View notes

Text

HARP 2 Refinance For Homeowners With Underwater Mortgages

In order to assist homeowners with underwater mortgages in refinancing their houses, the Federal Housing Finance Agency (FHFA) launched the Home Affordable Refinance Program (HARP) in 2009. HARP 2, an enhanced version of the 2012-introduced program, gives borrowers who are having trouble making their mortgage payments greater flexibility. We'll look more closely at the HARP 2 refinance in this blog post and how it can help homeowners with underwater mortgages.

What is an Underwater Mortgage

Let's start by defining an underwater mortgage. A homeowner who owes more on their mortgage than the value of their home at the time is said to be in an underwater mortgage position. A decrease in property prices, a change in the homeowner's financial condition, or other circumstances may be to blame for this.

It can be challenging to refinance a property when a homeowner has an underwater mortgage since conventional lenders could be reluctant to offer a refinancing loan. Herein is the value of HARP 2. With more lax conditions, the program enables qualified homeowners to refinance their underwater mortgage.

Benefits of HARP 2 Refinance

One of HARP 2's key advantages is that it enables homeowners to refinance their mortgage at a loan-to-value (LTV) ratio that is generally higher than what traditional lenders would permit. Homeowners may be able to refinance with an LTV ratio of up to 125% in some circumstances. This implies that homeowners may still be able to refinance and lower their monthly payments even if their home is worth less than what they owe on their mortgage.

Another advantage of HARP 2 is that it enables homeowners to refinance even with bad credit or a history of financial troubles. The program can assist homeowners who have had trouble getting approved for other forms of refinance loans because it has more lenient credit requirements than typical lenders.

Requirements to Qualify for HARP2 Refinance

Homeowners must fulfill specific eligibility conditions in order to be eligible for HARP 2. These consist of the following:

The mortgage must have originated on or before May 31, 2009, and it must be owned by or insured by either Fannie Mae or Freddie Mac.

The homeowner's mortgage payments must be up to date, with no more than one late payment in the previous 12 months and no late payments in the previous six months.

An LTV ratio of at least 80% is required.

The homeowner must demonstrate their ability to pay the increased mortgage payment.

Not all homeowners with underwater mortgages will be eligible for HARP 2; it is crucial to keep this in mind. But for those who do meet the requirements, the program can offer important advantages and support them in maintaining their homes.

To Sum Up

In conclusion, the HARP 2 program can offer assistance to homeowners who have underwater mortgages. It enables qualified homeowners to refinance their mortgages with less stringent conditions, such as a greater loan-to-value ratio and lenient credit standards. Homeowners must fulfill a number of qualifying criteria, such as having a mortgage owned by or insured by Fannie Mae or Freddie Mac, being current on their mortgage payments, and having an LTV ratio larger than 80%, in order to be eligible for HARP 2. HARP 2 can be a useful tool for homeowners who meet the requirements to lower their monthly mortgage payments while maintaining their houses.

#mortgages#gca mortgages#real estate#property#loans#fha loan#va loans#harp 2 program#bad credit score#homw owners#refinance#payments#united states#usa#first time home buyer#homebuyers#Underwater Mortgages#gustancho associates#gca mortgage#non qm loans#jumbo loans#conventional loans

3 notes

·

View notes

Text

How to Reduce EMI Burden on Your Personal Loan

A personal loan provides quick financial assistance for various needs, including medical emergencies, weddings, home renovations, and education expenses. However, high Equated Monthly Installments (EMIs) can become a financial burden, affecting your monthly budget and savings. Fortunately, there are several strategies to reduce your EMI burden and make loan repayment more manageable.

In this article, we will explore practical ways to lower your personal loan EMIs, factors affecting EMI amounts, and the best lenders offering flexible repayment options.

1. Understanding Personal Loan EMIs

An EMI (Equated Monthly Installment) is the fixed amount you pay every month towards your loan repayment. It consists of: ✅ Principal – The original amount borrowed. ✅ Interest – The cost of borrowing, calculated based on the loan amount, tenure, and interest rate.

The EMI amount depends on three key factors:

Loan Amount – Higher loans result in higher EMIs.

Interest Rate – A lower interest rate means a lower EMI.

Loan Tenure – A longer tenure reduces the EMI but increases the total interest paid.

Now, let's explore different ways to reduce your personal loan EMI burden.

2. Effective Ways to Reduce Your EMI Burden

2.1 Opt for a Longer Loan Tenure

Choosing a longer loan tenure spreads your repayment over more months, reducing your EMI amount. However, this also means you will pay more total interest over the loan tenure.

Example:

A ₹5,00,000 loan at 12% interest for 3 years = EMI of ₹16,607

A ₹5,00,000 loan at 12% interest for 5 years = EMI of ₹11,122

Best For: Borrowers looking for short-term relief in monthly expenses.

💡 Apply for a flexible tenure loan here: 👉 IDFC FIRST Bank Personal Loan

2.2 Make a Higher Down Payment or Part-Prepayment

If possible, make a lump sum payment towards your loan principal to reduce the EMI burden. This method helps you pay off the principal faster, lowering future EMIs.

How to do this?

Use bonuses, incentives, or tax refunds to prepay a portion of your loan.

Some lenders allow part-prepayment without extra charges.

💡 Best lenders offering part-prepayment options: 👉 Bajaj Finserv Personal Loan

2.3 Transfer Your Loan to a Lower Interest Rate Lender

If your current lender is charging high interest, consider a loan balance transfer to another bank or NBFC offering lower rates. This can significantly reduce your EMI.

Example: If your current loan interest rate is 14% p.a. and another bank offers 10.5% p.a., transferring your loan could save you a substantial amount in EMI payments.

💡 Best lenders for balance transfer: 👉 Tata Capital Personal Loan

2.4 Negotiate for a Lower Interest Rate

If you have a high credit score (750+), stable income, and good repayment history, you can negotiate with your lender for a lower interest rate, which directly reduces your EMI.

How to do this?

Request your lender for a reduced interest rate based on your financial profile.

If you’re a loyal customer, use that as leverage to negotiate better loan terms.

💡 Apply for low-interest loans here: 👉 Axis Finance Personal Loan

2.5 Opt for Step-Up EMI Plans

Some lenders offer step-up EMI plans, where your EMI starts at a lower amount and gradually increases as your income grows. This helps in managing the EMI burden in the early years.

Best for: Young professionals expecting salary hikes in the future.

💡 Lenders offering step-up EMI plans: 👉 Axis Bank Personal Loan

2.6 Choose a Fixed or Floating Interest Rate Wisely

Fixed interest rate loans have stable EMIs throughout the tenure.

Floating interest rate loans may change over time but can be lower when interest rates decrease.

If the market rates are expected to drop, consider a floating-rate loan to reduce EMI payments in the future.

💡 Best lenders for flexible interest rate options: 👉 InCred Personal Loan

2.7 Consolidate Multiple Loans into One

If you have multiple loans (personal loan, credit card debt, etc.), consider a debt consolidation loan. This helps in combining all loans into one, often with a lower interest rate and manageable EMI.

Benefits: ✅ Simplifies repayment with a single EMI. ✅ Reduces overall interest burden. ✅ Avoids multiple due dates and penalties.

💡 Apply for debt consolidation loans here: 👉 IDFC FIRST Bank Personal Loan

3. How to Avoid EMI Defaults & Late Payment Penalties

Even after reducing your EMI, ensure that you never miss a payment. Here’s how:

✔ Set Up Auto-Debit for EMIs – Link your loan EMI to auto-debit from your bank account to avoid missing payments. ✔ Keep an Emergency Fund – Save at least 3-6 months’ worth of EMI payments as a backup for emergencies. ✔ Monitor Your EMI Payments – Regularly check bank statements and loan accounts to track EMI deductions. ✔ Avoid Taking Multiple Loans – Too many loans can increase your financial stress. Borrow only what you need.

💡 For seamless EMI payments, set up auto-debit here: 👉 Personal Loan Auto-Debit Guide

Smart EMI Management for Financial Stability

Managing and reducing your EMI burden is key to maintaining financial stability while repaying your personal loan. The best strategies include:

✅ Opting for a longer tenure to reduce EMI size. ✅ Making part-prepayments to lower the outstanding principal. ✅ Transferring your loan to a lower interest rate lender. ✅ Negotiating with your lender for a better rate. ✅ Consolidating multiple loans into one for simplified repayment.

By applying these smart repayment techniques, you can ease your financial burden and repay your loan comfortably.

For the best personal loan options, check out: 👉 Apply for a Personal Loan

By planning your loan repayment wisely, you can enjoy lower EMIs, improved financial health, and stress-free loan management! 🚀

#Reduce EMI burden#Lower personal loan EMI#How to reduce EMI on loan#Personal loan EMI management#Ways to reduce loan EMI#Lower personal loan interest rate#EMI reduction strategies#Loan repayment tips#How to lower loan installment#Best ways to manage loan EMI#Personal loan balance transfer#Loan tenure and EMI impact#Debt consolidation loan#How to negotiate lower interest rates#Personal loan prepayment benefits#Fixed vs floating interest rates#Loan refinancing benefits#Personal loan repayment strategies#How to avoid EMI default#Best banks for low-interest personal loans#finance#personal loan online#personal loans#personal loan#bank#nbfc personal loan#fincrif#loan services#loan apps#personal laon

0 notes

Text

The Benefits of Using Loan Calculators in Real Estate

Loan calculators are invaluable tools for anyone involved in the real estate market. Whether you are a prospective homebuyer, a real estate investor, or a homeowner looking to refinance, loan calculators can provide you with essential information to make informed financial decisions. These online tools allow you to assess mortgage payments, interest rates, loan terms, and more. In this blog post, we will explore the benefits of using loan calculators in real estate and how they can help you maximize your financial outcomes.

One of the primary benefits of using loan calculators is the ability to determine affordability. By inputting specific financial data, such as your income, expenses, and desired loan amount, a loan calculator can calculate how much you can afford to borrow. This information is crucial in helping you set a realistic budget and avoid overextending yourself financially.

Additionally, loan calculators provide insights into the impact of interest rates on your monthly payments. By adjusting the interest rate input, you can see how different rates affect your loan payments. This allows you to compare various scenarios and choose the most favorable interest rate for your financial situation.

Loan calculators also help you understand the impact of loan terms on your overall cost. By adjusting the loan term input, you can see how longer or shorter loan terms affect your monthly payments and total interest paid. This knowledge empowers you to choose a loan term that aligns with your financial goals and minimizes the cost of borrowing.

Another benefit of using loan calculators is the ability to compare different loan options. If you are considering multiple lenders or loan products, a loan calculator can help you evaluate each option's affordability and suitability. By inputting the terms and conditions of each loan, you can compare the monthly payments, total interest paid, and other relevant factors. This allows you to make an informed decision and choose the loan that best meets your needs.

Furthermore, loan calculators are useful for refinancing decisions. If you are considering refinancing your mortgage, a loan calculator can help you determine if it's financially beneficial. By inputting your current loan details and comparing them to potential refinancing options, you can assess the savings in terms of lower interest rates or shorter loan terms. This helps you decide if refinancing is a viable option for you.

In conclusion, loan calculators are powerful tools that provide numerous benefits in the real estate industry. They assist with affordability assessments, comparing loan options, understanding the impact of interest rates and loan terms, and making informed refinancing decisions. By utilizing loan calculators, you can optimize your financial outcomes and ensure that you make sound decisions that align with your goals. So, take advantage of these online tools and empower yourself in your real estate journey.

2 notes

·

View notes

Text

A Real Helper in the Financial Crisis: Short Term Loans UK

If you meet the aforementioned requirements, you can still apply for short term loans UK even if you have a poor credit history due to defaults, arrears, foreclosure, missed or late payments, CCJs, IVAs, payment overdoes, skipping installments, or even bankruptcy. However, you are needed to repay the loan within the allotted time frame.

People who are living as paying guests or who don't have any assets to pledge can nevertheless benefit from rapid loans for benefit recipients. They are described as short term loans UK in this instance and you can apply for a loan without putting up any security. However, they remember that they must return the money in the shortest amount of time. In comparison to other financial products, the interest rate charged is a little high due to the short duration and unsecured nature of the product.

Payday loans UK can be applied for instantly online. To get the money granted, you must first choose the best loan option, complete a brief online application, and supply all necessary information. The short term loans direct lenders is securely sent into your bank account after loan approval. The list of things you can do with the money you earn includes paying for medical bills, power, groceries, home rentals, unexpected auto repairs, vacation costs, child's school or tuition fees, little home modifications, holding a party to honor your birthday, wedding costs, and so on.

Short Term Loans UK Direct Lender Extension

The short payback time is often the most problematic aspect of a short term loans UK direct lender for borrowers. Not everyone is eligible for the maximum time frame allowed, and even for those who are, it is occasionally impossible to repay the money in a timely manner. Lenders can assist you in this circumstance by extending your loan term or refinancing it under a new credit agreement. A loan extension is exactly what it sounds like: you agree to an extension of time to repay the loan. Naturally, this also implies that interest will keep accruing, raising the total amount you have to pay.

Why do people get so angry when unexpected surplus expenses occur? The reason is that because they don't save more money, they can have a lot of problems in the future. Short term loans UK are the sole option and the only true assistance in financial emergencies if it is necessary to take out a loan to cover all unexpected obligations. Every impaired person has access to this product at anytime, anyplace.

This is due to the fact that those who are severely suffering from physical or mental conditions are able to access additional funding through the aforementioned loan. Short term cash loans are typically provided to anyone who is reliant on social security benefits (DSS).

Additionally, there are standard eligibility requirements that must be met, including being a permanent citizen of the United Kingdom, residing in the same place for the previous 12 months, being at least 18 years old, maintaining an active checking account, and receiving DSS benefits.

3 notes

·

View notes

Text

Winter Home Buying in Minnesota: Why Cold Weather Can Be a Hot Opportunity

Winter might not seem like the ideal season to purchase a home, but for savvy buyers, it can actually be a great time to make a move. At KPT Mortgage Advisors, we help homebuyers navigate the seasonal real estate market with expert guidance, offering Mortgage Solutions for First-Time Homebuyers and Mortgage Refinance MN & WI options. If you're thinking about Buying A House In Minnesota this winter, here’s why it could be a smart decision.

The Advantages of Buying a Home in the Winter Market

Winter homebuying presents several benefits that can give you an edge:

Less Competition: Fewer buyers in the market mean reduced chances of bidding wars, giving you more negotiating power.

Motivated Sellers: Many homeowners selling in winter need to move quickly, which can lead to lower prices and better deals.

Faster Mortgage Processing: With fewer home purchases happening, lenders have more bandwidth to process loans efficiently.

Clear Home Inspection Conditions: Winter allows you to assess how well a home retains heat, its insulation quality, and whether ice dams or drafts are an issue.

Strategies for Winter Homebuyers

If you’re considering buying a house in Minnesota this winter, keep these strategies in mind:

Get Pre-Approved Early: Having a mortgage pre-approval strengthens your offer and speeds up the process.

Explore First-Time Buyer Programs: If you’re new to homeownership, our Mortgage Solutions for First-Time Homebuyers can help you access competitive rates and down payment assistance.

Be Flexible with Showings: Shorter daylight hours and winter weather can make scheduling home viewings challenging. Being flexible will help you see homes before other buyers.

Negotiate Closing Costs: Since sellers are often eager to close, they may be more willing to cover some of the closing costs or make necessary repairs.

Consider Refinancing Options: If you already own a home, winter is also a great time to explore Mortgage Refinance MN & WI options to secure a lower interest rate or better loan terms.

How KPT Mortgage Advisors Can Help

At KPT Mortgage Advisors, we specialize in helping buyers and homeowners find the best mortgage solutions year-round. Whether you’re a first-time homebuyer looking for the right loan program or a homeowner considering refinancing, we offer personalized guidance to fit your financial goals.

Get Started on Your Winter Home Buying Journey

Winter may seem like an unusual time to buy a home, but with the right approach, it can be the perfect opportunity to find your dream property at a great price. If you’re interested in buying a house in Minnesota, let KPT Mortgage Advisors guide you through the process with expert advice and tailored mortgage solutions.

Contact us today to explore your mortgage options and take the next step toward homeownership!

0 notes

Text

The Benefits of a Cash-Out Refinance: How to Fund Your Home Renovations

For homeowners seeking to upgrade their living space without taking on high-interest debt, a cash-out refinance offers a compelling solution. At Ace Mortgage Loan Corporation, clients are discovering how refinancing their homes can unlock valuable equity and make room for meaningful improvements. Whether it's updating a kitchen, creating a home office, or enhancing energy efficiency, this financial strategy helps fund renovations while potentially reducing borrowing costs. It also offers options for eligible borrowers to explore financing through VA home loan companies, which may provide additional benefits.

Understanding Cash-Out Refinance

A cash-out refinance replaces an existing mortgage with a new loan for a higher amount. The homeowner receives the difference in cash, which can then be used for anything from a kitchen remodel to energy-efficient upgrades. Many VA home loan companies offer this refinance option to eligible veterans and active-duty service members as part of their benefits.

How Does It Work?

When we apply for a cash-out refinance, our lender will assess the current value of our home and our outstanding mortgage balance. Based on this evaluation, they will determine how much equity we have built up. Typically, lenders allow us to access up to 80% of our home's value, minus what we still owe on the mortgage. The difference is given to us in cash, which we can then use for our renovation projects.

Benefits of a Cash-Out Refinance

Access to Lower Interest Rates

Compared to personal loans or credit cards, mortgage rates are typically lower. Homeowners who refinance into a new mortgage may enjoy reduced interest, making it more cost-effective to fund upgrades.

Consolidating Debt

A cash-out refinance can also offer us an opportunity to consolidate high-interest debts. By using the cash received from the refinance to pay off credit card balances or other loans, we can streamline our monthly payments into one manageable mortgage payment. This can simplify our financial obligations and potentially save us money in the long run.

Tax Benefits

Another advantage of cash-out refinancing is the potential tax benefits. In some cases, the interest paid on the new mortgage may be tax-deductible, especially if the funds are used for home improvements. It's crucial to consult with a tax advisor to understand how this applies to our specific situation, but this could be an added incentive to consider this refinancing option.

Funding Home Renovations with Cash-Out Refinance

Enhancing Property Value

By using a cash-out refinance to fund home renovations, we can significantly enhance the value of our property. Upgraded kitchens, modern bathrooms, and additional living space can make our home more attractive to potential buyers, should we decide to sell in the future. Even if selling isn't on our immediate horizon, knowing that our investment is increasing in value can provide peace of mind.

Personalizing Living Space

Renovations allow us to tailor our living spaces to better suit our lifestyle and preferences. Whether it's creating a home office, expanding the kitchen, or adding a deck for outdoor entertaining, a cash-out refinance gives us the financial means to turn our visions into reality. This personalization can greatly enhance our quality of life and enjoyment of our home.

Improving Energy Efficiency

Investing in energy-efficient upgrades can be a smart use of funds from a cash-out refinance. Installing new windows, upgrading insulation, or adding solar panels can reduce our utility bills and make our home more environmentally friendly. Over time, these improvements can lead to significant cost savings and increase the overall value of our property.

Considerations and Potential Drawbacks

Risks of Increased Debt

While a cash-out refinance can provide us with the funds needed for home improvements, it's essential to consider the potential risks. By increasing our mortgage balance, we are effectively taking on more debt. This could extend the time it takes to pay off our home and increase the total interest paid over the life of the loan. It's crucial to weigh these factors carefully and ensure that the benefits outweigh the costs.

Closing Costs

Just like with any mortgage transaction, a cash-out refinance involves closing costs. These can include appraisal fees, origination fees, and other expenses that can add up. It's important to factor these costs into our decision-making process and determine whether the benefits of the refinance justify the upfront expenses.

Impact on Credit Score

Applying for a cash-out refinance involves a credit inquiry, which can temporarily affect our credit score. Additionally, taking on more debt can impact our debt-to-income ratio, which lenders consider when evaluating creditworthiness. It's essential to maintain a healthy credit profile and ensure that we can comfortably manage the new mortgage payments.

Steps to Take Before Proceeding

Evaluate Our Financial Situation

Before pursuing a cash-out refinance, it's crucial to assess our financial situation. We should consider our current mortgage terms, interest rates, and the amount of equity we have in our home. It's also important to evaluate our long-term financial goals and ensure that a cash-out refinance aligns with our overall financial strategy.

Research Lenders

Not all lenders offer the same terms. Ace Mortgage Loan Corporation helps homeowners compare options and find a plan that suits their needs. Veterans and active-duty service members may also want to explore offers from VA home loan companies, which could provide additional flexibility and savings.

Consult with Financial Advisors

Speaking with a financial advisor or mortgage professional can help us make informed decisions. They can provide us with an objective assessment of our financial situation and offer tailored advice on whether a cash-out refinance is the right choice for us. Their expertise can be invaluable in navigating the complexities of refinancing and ensuring that we achieve our renovation goals efficiently and effectively.

For homeowners looking to fund renovations, a cash-out refinance presents a practical and cost-effective solution. With the potential for lower interest rates, added tax benefits, and increased property value, this financial tool continues to be a top choice among those planning substantial home improvements. Ace Mortgage Loan Corporation offers personalized support to guide homeowners through the refinancing process. Whether funding a new kitchen or consolidating debt, their team is equipped to help clients make confident, informed decisions. Those eligible for VA loans are also encouraged to explore options through VA home loan companies for added advantages. Now is the time to invest in your home’s future—and enjoy the upgrades you’ve been dreaming of. Get in touch with them today.

0 notes